In Proceedings of the 7th ACM SIGKDD International Conference on Knowledge Discovery and Data Mining (KDD-2001), August 2001.

Extracting Collective Probabilistic Forecasts from Web Games

David M. Pennock and Steve Lawrence

NEC Research Institute

4 Independence Way

Princeton, NJ 08540 USA

Finn Årup Nielsen

Informatics and Mathematical Modelling

Technical University of Denmark

DK-2800 Lyngby, Denmark

C. Lee Giles

Department of Computer Science and Engineering

Pennsylvania State University

University Park, PA 16801 USA

ABSTRACT

Game sites on the World Wide Web draw people from around the world

with specialized interests, skills, and knowledge. Data from the games

often reflects the players' expertise and will to win. We extract

probabilistic forecasts from data obtained from three online games:

the Hollywood Stock Exchange (HSX), the Foresight Exchange (FX), and

the Formula One Pick Six (F1P6) competition. We find that all three

yield accurate forecasts of uncertain future events. In particular,

prices of so-called ``movie stocks'' on HSX are good indicators of

actual box office returns. Prices of HSX securities in Oscar, Emmy,

and Grammy awards correlate well with observed frequencies of

winning. FX prices are reliable indicators of future developments in

science and technology. Collective predictions from players in the F1

competition serve as good forecasts of true race outcomes. In some

cases, forecasts induced from game data are more reliable than expert

opinions. We argue that web games naturally attract well-informed and

well-motivated players, and thus offer a valuable and oft-overlooked

source of high-quality data with significant predictive value.

ACM Categories and Subject Descriptors

H.2.8 [Database Management]: Database Applications - data mining

H.3.5 [Information Storage and Retrieval]: Online Information Systems-web-based services

J.4 [Computer Applications]: Social and Behavioral Sciences-economics

K.8 [Computing Milieux]: Personal Computing - games

Keywords

Collective probabilistic forecasts, World Wide Web games,

data mining, knowledge discovery, artificial markets, Hollywood Stock

Exchange, Foresight Exchange, Formula One Pick Six Competition

Introduction

Multiplayer games on the World Wide Web are growing in prevalence and

popularity, fueled in part by low operating costs and global

reach. Game players tend to be more knowledgeable and enthusiastic

about their game's topic than the public at large. For example, the

Hollywood Stock Exchange (HSX), a play-money market where traders bet

on the future success of movies and stars, draws heavily from among

film aficionados. In this paper, we investigate the use of such online

games as topic-focused sources of data with relatively high

signal-to-noise ratios, as compared to the web as a whole.

Section 2 discusses background and related work in

exploiting collective knowledge to generate forecasts.

Section 3 describes the three games under

study. Sections 4

and 5 evaluate the collective

competence of HSX players in predicting box office results and

entertainment award outcomes, respectively. In both cases, we find

that HSX forecasts are as accurate or more accurate than expert

judgments. Section 6 shows that prices on the

Foresight Exchange (FX) correlate strongly with observed outcome

frequencies for events of broad scientific and societal

interest. Section 7 examines the Formula One Pick

Six (F1P6) competition, showing that a simple weighting of

participants' predictions seems as reliable or more reliable than even

the official race odds. Section 8 discusses the more

general prospects of mining data and extracting knowledge from a

variety of online games and related sources.

Collective Forecasts

For decades, and across many disciplines, scientists have investigated

combining forecasts from multiple sources. Genest and

Zidek Genest86 and French French85 survey the

extensive literature on combining probability assessments from

multiple experts. Clemen Clemen89 reviews the equally

large (and related) body of work on combining forecasts; most studies

conclude that collective forecasts are indeed more accurate than

individual ones. Some of today's best machine learning methods are

so-called ensemble algorithms that combine classifications from

multiple learners to yield more robust classifications

[7]. Collaborative filtering algorithms or

recommender systems leverage community information about many

people's preferences in order to recommend items of interest (e.g.,

movies or books) to individuals [29].

Markets can also be thought of as combination devices.

Prices reflect information distributed among many traders, each with

direct monetary incentives to act on any pertinent

information. Informative prices often translate directly into accurate

forecasts of future events. For example, prices of financial options

are good probability assessments of the future prices of the

underlying assets [31]; prices in political stock

markets, like the Iowa Electronic Market (IEM),![[*]](footnote.png) can furnish better estimates of likely election outcomes than

traditional polls [11,12]; odds in horse races,

determined solely by how much is bet on which horses, match very

closely with the horses' actual frequencies of winning

[1,30,32,33,35];

and point-spread betting markets yield unbiased predictions of

sporting event outcomes [14]. Several studies demonstrate

that, in a laboratory setting, markets are often able to aggregate

information optimally [10,25,26,27].

In a game without monetary rewards, incentives to reveal information

presumably derive from entertainment value, educational value,

bragging rights, and/or other intangible sources. Our recent

investigations [22,23] conclude

that even market games show signs of collective competence. For

example, arbitrage opportunities on HSX (i.e., loopholes that allow

traders to earn a sure profit without risk) tend to disappear over

time, just as they do in real markets.

Sections 4,

5, and 6 show that

intangible rewards seem sufficient to drive forecast accuracy in

market games. Section 7 presents evidence that,

even without the ``carrot'' of monetary compensation, F1P6 players are

motivated enough to generate very accurate collective predictions of

Formula One racing outcomes.

can furnish better estimates of likely election outcomes than

traditional polls [11,12]; odds in horse races,

determined solely by how much is bet on which horses, match very

closely with the horses' actual frequencies of winning

[1,30,32,33,35];

and point-spread betting markets yield unbiased predictions of

sporting event outcomes [14]. Several studies demonstrate

that, in a laboratory setting, markets are often able to aggregate

information optimally [10,25,26,27].

In a game without monetary rewards, incentives to reveal information

presumably derive from entertainment value, educational value,

bragging rights, and/or other intangible sources. Our recent

investigations [22,23] conclude

that even market games show signs of collective competence. For

example, arbitrage opportunities on HSX (i.e., loopholes that allow

traders to earn a sure profit without risk) tend to disappear over

time, just as they do in real markets.

Sections 4,

5, and 6 show that

intangible rewards seem sufficient to drive forecast accuracy in

market games. Section 7 presents evidence that,

even without the ``carrot'' of monetary compensation, F1P6 players are

motivated enough to generate very accurate collective predictions of

Formula One racing outcomes.

The Games

The Hollywood Stock Exchange

The Hollywood Stock Exchange (HSX)

is a popular online market game, with approximately 400,000 registered

accounts. New accounts begin with H$ two million in ``Hollywood

dollars''. Participants can buy and sell movie stocks, star bonds,

movie options, and award options. The current top portfolio is worth

just over H$1 billion. High ranking portfolios are actually sold at

auction on Ebay for real money on

a regular basis. Based on these sales, the ``exchange rate'' seems to

be approximately H$1 million to US$1, with the rate increasing for

higher ranked portfolios. HSX is beginning to offer new investment

opportunities backed with real money. For example, HSX investors could

purchase shares in the movie American Psycho for H$1 million

each; these shares paid off about US$1 for every US$5 million of the

movie's box office proceeds. HSX cofounder Max Keiser hosts a weekly

radio broadcast in Los Angeles, and appears regularly on NBC's

Access Hollywood to discuss HSX information. HSX also sponsors

a booth at the Sundance Film Festival, and holds an annual Oscar party

in Hollywood. Media reports suggest that HSX prices are taken

seriously by some Hollywood insiders.

Although the current price of any HSX movie stock is based on the

collective whims of HSX traders, the value of the stock is ultimately

grounded in the corresponding movie's performance at the box

office. Specifically, after the movie has spent four weeks in release,

the stock delists and cashes out: shareholders receive H$1 per share

for every US$1 million that the movie has grossed up to that point in

the US domestic market, as reported by ACNielsen EDI,

Inc. Traders buy (resp., short

sell) stocks that they believe underestimate (overestimate) the

movie's eventual performance. The current price, then, is a collective

forecast of the movie's four-week box office

returns.

The prices of some stocks adjust after their first weekend in wide,

national release. On Friday, trading in the stock is halted; on

Sunday, the price adjusts to H$2.9 times the movie's weekend box

office numbers (in US$ millions). In this case, the stock's price

prior to wide release is the HSX traders' forecast of 2.9 times the

movie's opening weekend proceeds. The 2.9 factor is meant to project

the movie's four week total based on its opening weekend results.

Occasionally, HSX offers ``award options'' associated with particular

entertainment awards ceremonies--for example, the 72nd Annual Academy

Awards, or Oscars, sponsored by the Academy of Motion Picture

Arts and Sciences in 2000. Five options, corresponding to the five

award nominees, are available within each award category (for example,

Oscar award options were available for each of the eight major Oscar

categories of best picture, best actor, best actress, best supporting

actor, best supporting actress, best director, best original

screenplay, and best adapted screenplay). Within each category, the

winning option cashes out at H$25, and the other four cash out at

H$0. Before awards are announced, an option's price can be

interpreted as its estimated likelihood of winning. For example, when

Kevin Spacey's price was twice that of Denzel Washington, the

consensus of HSX opinions was that Spacey was roughly twice as likely

to win as Washington. By normalizing prices within each category,

likelihoods can be converted into probabilities.

The Foresight Exchange

Hanson Hanson99,Hanson95 proposes what he calls an

Idea Futures market, where participants trade in securities

that pay off contingent on future developments in science, technology,

or other arenas of public interest. For example, a security might pay

off US$1 if and only if a cure for cancer is discovered by a certain

date. He argues that the reward structure of such a market encourages

honest revelation of opinions among scientists, yielding more accurate

forecasts for use by funding agencies, public policy leaders, the

media, and other interested parties. The concept is operational as a

web game called the Foresight Exchange

(FX). There are

currently on the order of 3000 registered participants and 200 active

claims. Players start with an initial amount of ``FX bucks'' and

receive an allowance every week, up to a certain maximum. Participants

can buy and sell existing claims, or submit their own claims. Each

claim is assigned a judge to arbitrate ambiguous wording, and to

ultimately determine whether the claim is true or not on the judgment

date. Claims range from technical (e.g., FX$1 if and only if an

algorithm for three satisfiability is developed with a particular

runtime complexity by the year 2020) to sociopolitical (e.g., FX$1 if

and only if Japan possesses nuclear missiles by 2020) to irreverent

(e.g, FX$1 if and only if Madonna names her first child Jesus). The

developers of the site intend for the prices of these claims to be

interpreted as assessments of the probabilities of the various events.

The Formula One Pick Six Competition

Formula One (F1) is one of the prime international race car

competitions. Drivers compete in approximately 16 races during a

season, accumulating points according to how well they place within

each race. The sport draws a large and avid following, especially in

Europe. Betting on the sport is also quite popular. A variety of

bookmakers, both online and off, support bets on the outcomes of

individual F1 races and on the results of an entire season. Media

coverage of the sport is fairly extensive, including a variety of

informative websites (e.g., http://www.motorsport.com/).

Formula One Pick Six (F1P6) is an email- and web-based competition for

predicting F1 outcomes. The game has been in existence

for a number of years, and currently has several thousand registered

participants. No monetary reward is associated with the F1P6

competition. The goal is to correctly forecast the top six drivers of

each race. Participants receive a score based one how well their

ranking of drivers matches the actual result. For each correct

driver-place prediction, they receive 10 points. For each driver

prediction that is one place off, they receive 6 points. For each

driver prediction that is 2, 3, 4, or 5 places off, they receive 4, 3,

2, or 1 points, respectively. Drivers that finish in seventh place and

below are disregarded. Wasserman [34] describes

statistical analyses of the first three years (1994-1996) of the

competition.

Box office forecasts: HSX movie stocks

In this section, we evaluate HSX movie box office forecasts according

to several error metrics. We also investigate the benefit of augmenting

game data with outside information to boost prediction quality.

Recall that, before a movie's opening weekend, its price on HSX is an

estimate of 2.9 times its weekend proceeds. We collected the halt

prices  (Friday morning's prices) and adjust prices

(Friday morning's prices) and adjust prices  (2.9

times the actual return) from HSX for 50 movies opening during the

period March 3, 2000 to September 1, 2000.

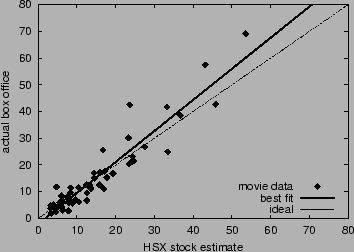

Figure 1 plots the actual box

office return

(2.9

times the actual return) from HSX for 50 movies opening during the

period March 3, 2000 to September 1, 2000.

Figure 1 plots the actual box

office return  versus the HSX estimate

versus the HSX estimate  for each

movie. We measure accuracy of the forecasts according to four metrics:

(1) correlation between estimate and actual, (2) average absolute

error, (3) average percent error, and (4) slope of the best-fit line

to the data.

Table 1 reports these error

measurements for baseline HSX data. Without any preprocessing (e.g.,

boosting, filtering, or learning), HSX forecasts are remarkably

accurate. Game players--at least collectively--appear to be

knowledgeable about the prospects of upcoming movies and are

sufficiently well-motivated to reveal their information in the context

of the game, even without much prospect for tangible compensation.

for each

movie. We measure accuracy of the forecasts according to four metrics:

(1) correlation between estimate and actual, (2) average absolute

error, (3) average percent error, and (4) slope of the best-fit line

to the data.

Table 1 reports these error

measurements for baseline HSX data. Without any preprocessing (e.g.,

boosting, filtering, or learning), HSX forecasts are remarkably

accurate. Game players--at least collectively--appear to be

knowledgeable about the prospects of upcoming movies and are

sufficiently well-motivated to reveal their information in the context

of the game, even without much prospect for tangible compensation.

Figure 1:

Accuracy of HSX movie stock forecasts to predict opening

weekend box office returns. The dashed line corresponds to ideal accuracy;

the solid line is the best linear fit.

|

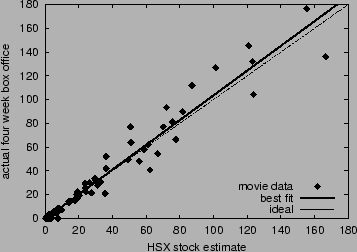

Next, we evaluate HSX predictions of four-week total box office

proceeds. After a movie stock on HSX adjusts (or if it does not

adjust), its price becomes a forecast of the movie's four-week box

office total  . We gathered the delist prices and the prices

three weeks before delist

. We gathered the delist prices and the prices

three weeks before delist  for 109 movies between March 3, 2000

to September 1, 2000. Figure 2

graphs versus for each movie. The correlation is 0.978,

the best-fit line's slope is 1.04, and the average error is 4.01. The

average percent error is undefined (infinite), since a few small

movies apparently did not earn any measurable amount of money.

for 109 movies between March 3, 2000

to September 1, 2000. Figure 2

graphs versus for each movie. The correlation is 0.978,

the best-fit line's slope is 1.04, and the average error is 4.01. The

average percent error is undefined (infinite), since a few small

movies apparently did not earn any measurable amount of money.

Figure 2:

Accuracy of HSX movie stock forecasts to predict four week total

box office returns. The dashed line corresponds to ideal

accuracy; the solid line is the best linear fit.

|

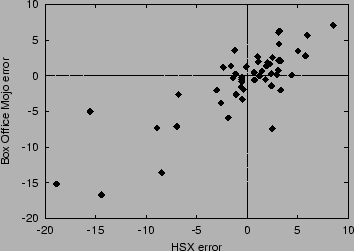

We also recorded the forecasts of opening weekend returns from movie

expert Brandon Gray of Box Office Mojo. Table 1

compares the accuracy of Box Office Mojo predictions to HSX

predictions. The two forecasts are of comparable quality--Box Office

Mojo performed 4% better than HSX in terms of average percent

error. In fact, the two sources make similar

errors. Figure 3 plots the correlation between

HSX errors and Box Office Mojo errors. Both sources overestimate a

larger fraction of movies; but when they do underestimate, they are

off by a greater amount. This occurs because both tend to

underestimate the best box office performers. The correlation in

errors between HSX and Box Office Mojo is 0.818. The two estimates may

result from overlapping sources of evidence--for example, it is

possible that Brandon Gray observes HSX prices, and/or that some HSX

traders read Box Office Mojo forecasts.

Figure 3:

Correlation between HSX opening weekend forecast errors and

Box Office Mojo forecast errors.

|

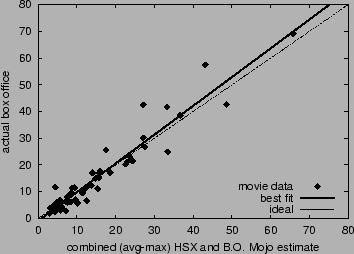

We investigate combining data from HSX and Box Office Mojo to sharpen

predictions. The simplest method--averaging the two

estimates--results in increased correlation, decreased average error,

and decreased percent error, as reported in

Table 1. Since both sources

underestimate big box office winners, we tried a second combination

procedure that returns the average of the two forecasts if that

average is less than twenty-five, otherwise returning the maximum of

the two forecasts. This ``avg-max'' combination gave the most accurate

predictions according to all four metrics (see

Table 1). Figure 4

graphs box office numbers versus this combined estimate. Without more

data, we hesitate to employ more sophisticated learning and boosting

techniques lest we begin to overfit; on the other hand, given access

to training and test data over a larger time frame, such methods will

likely become warranted.

Table 1:

Accuracy of HSX, Box Office Mojo, and combined forecasts of

opening weekend box office returns. Accuracy metrics are

correlation, average error, average percent error, and slope of

the least-squares best-fit line.

| |

corr |

avg err |

avg %err |

fit |

| HSX |

0.940 |

3.57 |

31.5 |

1.16 |

| BOMojo |

0.945 |

3.31 |

27.5 |

1.10 |

| avg |

0.950 |

3.16 |

27.0 |

1.15 |

| avg-max |

0.956 |

2.90 |

26.6 |

1.08 |

Figure 4:

Accuracy of combined HSX and Box

Office Mojo forecasts to predict opening

weekend box office returns. The dashed line

corresponds to ideal accuracy;

the solid line is the best linear fit.

|

Combining forecasts works best when individually accurate sources make

uncorrelated errors [7]. Since HSX and Box Office Mojo

exhibit dependent errors, the gain from merging data, while

appreciable, is relatively small. Identifying alternative sources that

yield independent forecasts will be a key component of any data

combination strategy. Some candidate sources to explore include chat

board postings, query logs, press coverage, movie reviews, and link

structure on the web.

Entertainment Award Forecasts: HSX Award Options

In the 2000 HSX Oscar options market, as it turns out, each nominee

with the highest final price in its category did indeed win an Oscar.

The Wall Street Journal, amid controversy, published a poll of actual

Academy voters days before the Oscar awards ceremony; their report

correctly forecasted only seven out of eight winners.

Beyond predicting the most likely winner, we investigate how

accurately HSX award option prices reflect all likelihoods of

winning. For example, if prices are accurate, then among all options

with a normalized price of H$0.1, about one in ten should end up

winning. Our accuracy analysis is similar to that conducted for horse

races

[1,30,32,33,35]

and other sports betting markets involving real money. We collected

prices of award options associated with the 2000 Oscars,

Grammies, and Emmies, for a total of

135

options. Grammy options (nine categories) and Emmy options (ten

categories) functioned exactly as Oscar options, though winning Grammy

options paid out H$42 instead of H$25.

Figure 5:

Accuracy of the HSX award options market. Points display

observed frequency versus average normalized price for buckets of

similarly-priced options. The dashed line where frequency equals

price corresponds to ideal accuracy.

![\begin{figure}

\begin{center}

\centerline{\scalebox{0.65}{\epsfig{file=hsx-a...

...udegraphics[width=14cm]{hsx-oscar-arbitrage.eps}

\end{center}

\end{figure}](img11.png) |

Prices were recorded just before the markets closed, and before

winners were announced. We sorted the options by price, and grouped

them into six buckets. We placed the same number of options (16)

in every bucket, under the constraint that every bucket include at

least one winning option. We computed the average normalized price of

options within each bucket, and the observed frequency within

each bucket, or the number of winning options divided by the number of

options. Figure 5 plots each

bucket's observed frequency versus its average normalized price. If we

model options as independent Bernoulli trials, then, in the limit as

the number of options goes to infinity, completely accurate prices

would imply that bucket points fall on the line  , where observed

frequency equals price. Error bars display 95% confidence intervals

under the independent Bernoulli trials assumption. Specifically, the

lower error bound is the 0.025 quantile of a Beta distribution

corresponding to the observed number of successes (wins) and trials in

the bucket, and the upper error bound is the 0.975 quantile. The Beta

distribution is the correct posterior distribution over frequency,

assuming a uniform prior. The length of an error bar decreases as the number of

options in the bucket increases. The independence assumption is an

idealization, since options within a single award category are

actually mutually exclusive. The closeness of fit to the line

can be considered a measure of the accuracy of HSX prices.

, where observed

frequency equals price. Error bars display 95% confidence intervals

under the independent Bernoulli trials assumption. Specifically, the

lower error bound is the 0.025 quantile of a Beta distribution

corresponding to the observed number of successes (wins) and trials in

the bucket, and the upper error bound is the 0.975 quantile. The Beta

distribution is the correct posterior distribution over frequency,

assuming a uniform prior. The length of an error bar decreases as the number of

options in the bucket increases. The independence assumption is an

idealization, since options within a single award category are

actually mutually exclusive. The closeness of fit to the line

can be considered a measure of the accuracy of HSX prices.

We compare HSX prices of Oscar options to reported likelihood

assessments from five columnists at the Hollywood Stock Brokerage and

Resource (HSBR), a fansite of

HSX. We use the logarithmic scoring rule to rate the market and the

columnists. The logarithmic score is a proper scoring rule

[36], and is an accepted method of evaluating probability

assessors. When experts are rewarded according to a proper score, they

can maximize their expected return by reporting their probabilities

truthfully. Additionally, more accurate experts can expect to earn a

higher average score than less competent experts. Scores are computed

separately within each award category, then averaged. Index the five

nominees in a category

. Let

. Let  if and only if

the

if and only if

the  th nominee wins, and

th nominee wins, and  otherwise. let

otherwise. let

be the market's or columnist's reported probabilities for the

five nominees. Then the assessor's score for the current category is

be the market's or columnist's reported probabilities for the

five nominees. Then the assessor's score for the current category is

. Expert assessments were

reported on February 18,

2000. Table 2 gives the average

scores for the HSX market, the five columnists, and the consensus of

the columnists. Higher scores are better, with 0 the maximum and

negative infinity the minimum. Only one of the five experts scored

appreciably better than the market on February 18. HSX's score

increased almost continuously from the market's open on February 15 to

the market's close on March 26. By February 19, the market's score had

surpassed all of the scores for all five experts and for their

consensus.

. Expert assessments were

reported on February 18,

2000. Table 2 gives the average

scores for the HSX market, the five columnists, and the consensus of

the columnists. Higher scores are better, with 0 the maximum and

negative infinity the minimum. Only one of the five experts scored

appreciably better than the market on February 18. HSX's score

increased almost continuously from the market's open on February 15 to

the market's close on March 26. By February 19, the market's score had

surpassed all of the scores for all five experts and for their

consensus.

Table 2:

Accuracy of HSX Oscar forecasts and

HSBR columnists' forecasts, evaluated

according to average logarithmic score.

Higher (less negative) scores are better.

| forecast source |

avg log score |

| Feb 18 HSX prices |

-1.08 |

| Feb 19 HSX prices |

-0.854 |

| Tom |

-1.08 |

| Jen |

-1.25 |

| John |

-1.22 |

| Fielding |

-1.04 |

| DPRoberts |

-0.874 |

| columnist consensus |

-1.05 |

Science and Technology Forecasts: The Foresight Exchange

Like HSX award options, FX prices constitute collective probability

assessments of future events. To determine how accurate these

assessment are, we collected historical price information for all

retired (completed) claims as of September 8, 2000. Of these, we

retained only the 172 that were binary (i.e., paid off if and only if

some true-or-false event occurred).

We recorded the price of each claim 30 days before it expired. A total

of 161 claims were active for at least 30 days, and thus qualified for

this data set. We sorted the claims by their 30-day-before-expiration

price, grouped them into six buckets of size 17 (under the constraint

that every bucket contain at least one winning claim), and computed

the average price and observed frequency for each bucket.

Figure 6:

Accuracy of the Foresight Exchange market. Prices are 30

days before claim expiration. Points display observed frequency

versus average price. The dashed line corresponds to ideal

accuracy.

![\begin{figure}

\begin{center}

\centerline{\scalebox{0.65}{\epsfig{file=if-ac...

...udegraphics[width=14cm]{hsx-oscar-arbitrage.eps}

\end{center}

\end{figure}](img23.png) |

Figure 6

graphs the results. Prices correlate well with observed outcome

frequencies.

Error bars show 95% confidence intervals based on the assumption that

claims are independent Bernoulli trials with a uniform prior over

frequency.

Formula One Forecasts: F1P6

The reward structure in the F1P6 competition is quite different than

in HSX, FX, or the F1 betting market. Correctly predicting an

improbable event yields no more points than correctly predicting a

likely event. One might expect that competitors would consistently

choose the six most probable winners. But this strategy may not always

be optimal. By choosing only the best drivers, a participant is not

likely to differentiate himself or herself from the pack (unless

everyone reasons this way). For example, Kaplan and Garstka

Kaplan01 show that, under some conditions, picking the top

seeds in an NCAA basketball tournament pool does not always maximize

the chances of winning. Moreover, when no money is involved, a player

may not gain much sense of accomplishment when he or she simply picks

the top six drivers, even if he or she does win. Thus, the nature of

the competition may induce some strategic incentives to carefully pick

a few upsets.

Figure 7:

For each race in 1999, the fraction of F1P6 participants

that predicted Michael Schumacher to win.

Dots near the top of the chart indicate the races

that he actually competed in.

![\begin{figure}

\begin{center}

\centerline{\scalebox{0.45}{\epsfig{file=Finn-...

...udegraphics[width=14cm]{hsx-oscar-arbitrage.eps}

\end{center}

\end{figure}](img24.png) |

Individuals in the competition are not always fully informed and

rational. For example, when one of the best drivers--Michael

Schumacher--was absent from some races due to injury, several of the

F1P6 players continued to pick him to win. Figure 7 shows

the races that Schumacher competed in during 1999, and the fraction of

participants that predicted him to win. The observed behavior may be

due to a lack of information, or because players skip races, in which

case their previous predictions are carried over. However, carry-over

occurs only once.

Although individuals clearly make faulty predictions, we examine

whether collective information in the game is sufficient to yield

accurate overall predictions. We obtained the predictions of all F1P6

participants from the competition web site for 32 of 41 races held

from 1999 through June 10, 2001. Unlike the other two games investigated, F1P6

does not contain a natural ``price'' statistic that summarizes the

consensus of opinions of all participants. In an attempt to identify a

good summary statistic, we tried four different ways of scoring the

drivers according to the participants' predictions.

- linear scoring (6-5-4-3-2-1)

- F1-style scoring (10-6-4-3-2-1)

- flat scoring (1-1-1-1-1-1)

- winner scoring (1-0-0-0-0-0)

For example, linear scoring assigns to a driver six points for every

F1P6 participant that predicts that driver to finish in first place,

five points for every participant that predicts the driver to finish in

second, and so on. We normalized drivers' scores to obtain a

pseudo-probability associated with each scoring rule.

We collected the actual race results from Atlas F1 and Gale Force F1. We sorted driver-races by score, grouped them

into buckets of constant size, and computed the average scores and

observed frequencies in all buckets. To control against data snooping,

we performed an initial analysis on the 1999 races only. On this data,

linear scoring performed best, with F1-style scoring a close second;

flat scoring and winner scoring performed poorly. The remainder of

results in this section refer to all races from 1999 through June 10,

2001. Figure 8 plots the bucket points

obtained from linear scoring. Error bars are 95% confidence

intervals, under the independent Bernoulli trials assumption. The

figure indicates that linear scores are good estimates of the actual

frequencies of race outcomes. Figure 9 shows

the accuracy of F1-style scoring; this method also appears to yield

accurate psuedo-probabilities. Figures 10

and 11 display the same plots for flat

scoring and winner scoring, respectively; neither of these scoring

methods perform well. These results are consistent with our initial

1999-only analysis, providing a measure of confidence that results are

robust.

Figure 8:

Accuracy of the F1P6 competition.

Points display observed frequency versus linear score.

The dashed line corresponds to ideal accuracy.

![\begin{figure}

\begin{center}

\centerline{\scalebox{0.65}{\epsfig{file=f1-li...

...udegraphics[width=14cm]{hsx-oscar-arbitrage.eps}

\end{center}

\end{figure}](img25.png) |

Figure 9:

Observed frequency versus F1-style score.

![\begin{figure}

\begin{center}

\centerline{\scalebox{0.65}{\epsfig{file=f1-lo...

...udegraphics[width=14cm]{hsx-oscar-arbitrage.eps}

\end{center}

\end{figure}](img26.png) |

Figure 10:

Observed frequency versus flat score.

![\begin{figure}

\begin{center}

\centerline{\scalebox{0.65}{\epsfig{file=f1-fl...

...udegraphics[width=14cm]{hsx-oscar-arbitrage.eps}

\end{center}

\end{figure}](img27.png) |

Figure 11:

Observed frequency versus winner score.

![\begin{figure}

\begin{center}

\centerline{\scalebox{0.65}{\epsfig{file=f1-wi...

...udegraphics[width=14cm]{hsx-oscar-arbitrage.eps}

\end{center}

\end{figure}](img28.png) |

In the case of F1 racing, we have access to a real-money

market--namely the F1 betting market--that naturally lends itself to

comparison with the F1P6 game results. We collected archive betting

odds from Atlas F1 for 39 of 41 races held from 1999 through June 10,

2001.

The odds do not reflect a balanced market, since gamblers can only bet

for a particular driver, not against. In order to ensure a profit,

bookmakers purposefully set the odds such that the corresponding

probabilities sum to greater than one. We found the average excess

probability to be 0.23. We normalized the odds, although it is

possible that bookmakers overstate probabilities in some nonlinear

way. There are some symmetric gambles available, where bettors choose

which of two drivers will fare better. These bets had smaller excess

probabilities (about 0.05), but there were not enough to determine

probabilities across the entire field of drivers. Again, we sorted by

probability (normalized odds), binned the data (in buckets of constant

size), and computed average probability and observed frequency.

Figure 12 graphs the results along with 95%

confidence error bars.

Figure 12:

Accuracy of the bookmaker odds from Atlas F1.

Points display observed frequency versus normalized odds.

![\begin{figure}

\begin{center}

\centerline{\scalebox{0.65}{\epsfig{file=f1-at...

...udegraphics[width=14cm]{hsx-oscar-arbitrage.eps}

\end{center}

\end{figure}](img29.png) |

Table 3 compares the average logarithmic score

for the four types of F1P6 psuedo-probabilities and for the F1 betting

odds, computed over the 30 races for which our data sets

overlap. Perhaps surprisingly, F1-style scoring and linear scoring

outperformed the official odds, if only slightly. Note, however, that

the bookmaker odds may be purposefully biased in a nonlinear fashion.

Table 3:

Accuracy of psuedo-probabilities from

F1P6 and normalized odds from Atlas F1, evaluated

according to average logarithmic score.

Higher (less negative) scores are better.

| forecast source |

avg log score |

| F1P6 linear scoring |

-1.84 |

| F1P6 F1-style scoring |

-1.82 |

| F1P6 flat scoring |

-2.03 |

| F1P6 winner scoring |

-2.32 |

| Atlas F1 normalized odds |

-1.86 |

It is interesting to note that the pattern of results for F1-style

scoring (Figure 9) is very similar to that for

the betting odds (Figure 12). Ideally, we

would like a model of prediction strategies [19] and race

outcomes that explains why F1-style scoring mimics the odds, why

F1-style and linear scoring yield good predictions, and why the other

two scoring methods fail. At this point, however, we have not

formalized any explanations.

We tested only four scoring rules among a class of six dimensional

weighted averaging rules, in part to avoid overfitting our limited

data. With more training and test data, learning the vector of

weights, or learning other functional mappings from F1P6 votes to

psuedo-probabilities, begins to make sense. One might also explore

combining F1P6 and betting odds data, or combining with data from

other games, web sites, or other sources.

Data Mining from Online Games: Implications and Applications

A growing number of games and markets on the web provide vast amounts

of data reflecting the interactions of millions of people around the

world. Each source offers the opportunity to infer something about the

players involved and the knowledge they possess. Data mining

algorithms--typically fast algorithms for extracting knowledge from

massive quantities of data [8,28]--seem

particularly well suited for the job. In this work, we employed simple

extraction algorithms to obtain probabilistic forecasts of real-world

events. Our results can be seen as statistical validation of the

underlying quality of data from online games. The games themselves

appear to serve as a mechanism for collecting, merging, and cleaning

data from human experts, naturally handling some of the more difficult

steps in a typical data mining application [4,20]. Yet

we expect room for improvement with the use of more sophisticated

algorithms and data fusion techniques.

For example, with access to user-specific data, predictions could be

improved by weighting users according to inferred measures of

reliability or expertise, filtering out ``noisy'' users, and

identifying and removing users attempting to manipulate the game. Game

forecasts could also be boosted with information from outside

sources. For example, baseline HSX box office predictions could

benefit from additional data from expert forecasts, statistical

sampling, critical reviews, actor popularity, advertising budgets,

number of screens playing, discussion boards, newsgroups, search

queries [2], distribution of inbound hyperlinks

pointing to movie homepages, web community sizes [9], etc.

More detailed analysis of game dynamics can actually lead to

algorithms for identifying and pinpointing the introduction of new

knowledge into the public consciousness. For example, in August 1996,

the rapid increase in the price of a bet on FX that extraterrestrial

life will be discovered can be traced to

news at the time that fossils were potentially identified in a Martian

meteorite [21]. Similarly, two sequential decreases in the

price of a bet on the (real-money) Iowa Electronic Market that Rudy

Giuliani will win the 2000 US Senate election in New York can be

correlated with two announcements during his campaign: first that he

had prostate cancer, and later that he was dropping out of the race.

In non-market games like F1P6, generating probabilistic forecasts

requires more explicit data manipulation, since a natural price

statistic is not available. In this paper, we tried weighted voting

procedures as a first step, finding that a linear combination seems to

work well, though more advanced machine learning and data mining

techniques are certainly applicable. Additionally, with a model of how

people play the game [19], one can infer the maximum

likelihood opinion of each user, then combine results using known

belief or forecast aggregation methods [3,15].

Inevitably, multiple sites will focus on interrelated topics, and

extraction algorithms will benefit from combining data sources while

accounting for correlations. More general online communities, for

example chat boards or newsgroups, feature some of the same benefits

as game sites--namely dedicated and knowledgeable participants often

willing to divulge information--though leveraging this more free-form

data will require more complex processing algorithms.

An obvious path for applications is to mine information from existing

games. Alternatively, organizations may set up their own online games

as a mechanism for gathering data on particular subjects of interest

or concern, perhaps as an alternative to costly market research

[16]. While Internet polls are notoriously skewed

toward an unrepresentative (more educated, more wealthy, more

conservative) demographic, it appears that web games actually benefit

from the bias within their niche audiences. Perhaps the difference

arises because, while polls typically ask questions of the form ``what

do you want?'', these games pose questions of the form ``what do you

think will happen?'' to an attentive and knowledgeable

audience. However, if corporations begin to take game data seriously,

players may feel wary about privacy issues and what information they

are revealing for free and to whom. Moreover, once data is being used

for consequential decisions, incentives to manipulate the game

increase, and good mechanisms for filtering or controlling

manipulation will be essential.

The World Wide Web fosters large-scale group activities of all sorts,

from competing in games, to trading in markets, to competing in market

trading games. We find that, beyond their entertainment and

commercial value, these sites can be valuable resources for inferring

predictions about real-world events. We show that HSX prices are

informative signals for movie box office results and entertainment

award outcomes--as accurate or more accurate than expert opinions. FX

prices reliably forecast true outcome frequencies for scientific and

societal questions. The combined judgments of F1P6 competitors are

equally or better aligned with actual race outcomes than the official

betting odds.

In both economics [24] and decision science

[6,36] it is known that appropriate monetary

reward structures can induce people to reveal their inside information

and expert knowledge. Our results provide evidence that well-designed

games also provide sufficient incentives for people to divulge their

information. In this context, the players' motivations derive from

their competitive spirit and the value of entertainment, rather than

directly from consumable (e.g., monetary) compensation. In all three

games studied, participants appear to be (collectively) knowledgeable,

and to take winning seriously enough to reveal that knowledge

indirectly through their play. Such online games act as a sink for

specialized information from experts. We believe that, in contrast to

the low signal-to-noise ratio on web as a whole, many online games are

good sources for targeted mining of pertinent and useful data.

We thank Yan Chen, Gary Flake, Robin Hanson, Chris Meek, Forrest

Nelson, Melissa Perrot, William Walsh, Mike Wellman, and the anonymous

reviewers for advice, encouragement, insightful comments, and pointers

to related work. Thanks to Eric Glover for research and programming

assistance. Thanks to James Pancoast and ``Jimmy Impossible'' from the

Hollywood Stock Brokerage and Resource (http://www.hsbr.net/), a

fansite of HSX; Ken Kittlitz from the Foresight Exchange; Paul

Winalski and John Francis from the F1P6 competition; and João Paulo

Lopes da Cumba from the Formula One Results and Information eXplorer

(http://www.forix.com/).

- 1

-

M. M. Ali.

Probability and utility estimates for racetrack bettors.

Journal of Political Economy, 85(4):803-816, 1977.

- 2

-

D. Beeferman and A. Berger.

Agglomerative clustering of a search engine query log.

In Sixth International Conference on Knowledge Discovery and

Data Mining, pages 407-416, 2000.

- 3

-

R. T. Clemen.

Combining forecasts: A review and annotated bibliography.

International Journal of Forecasting, 5:559-583, 1989.

- 4

-

W. W. Cohen, H. Kautz, and D. McAllester.

Hardening soft information sources.

In Sixth International Conference on Knowledge Discovery and

Data Mining, pages 255-259, 2000.

- 5

-

Weighted least sum of squares regression.

In C. Croarkin, P. Tobias, and W. Guthrie, editors, NIST/SEMATECH Engineering Statistics Internet Handbook.

http://www.itl.nist.gov/div898/handbook/pmd/

[0]section1/pmd143.htm.

- 6

-

B. de Finetti.

Theory of Probability: A Critical Introductory Treatment,

volume 1.

Wiley, New York, 1974.

- 7

-

T. G. Dietterich.

Machine learning research: Four current directions.

Artificial Intelligence Magazine, 18(4):97-136, 1997.

- 8

-

U. Fayyad, G. Piatetsky-Shapiro, and P. Smyth.

Knowledge discovery and data mining: Towards a unifying framework.

In Second International Conference on Knowledge Discovery and

Data Mining, 1996.

- 9

-

G. W. Flake, S. Lawrence, and C. L. Giles.

Efficient identification of web communities.

In Sixth International Conference on Knowledge Discovery and

Data Mining, pages 150-160, 2000.

- 10

-

R. Forsythe and R. Lundholm.

Information aggregation in an experimental market.

Econometrica, 58(2):309-347, 1990.

- 11

-

R. Forsythe, F. Nelson, G. R. Neumann, and J. Wright.

Anatomy of an experimental political stock market.

American Economic Review, 82(5):1142-1161, 1992.

- 12

-

R. Forsythe, T. A. Rietz, and T. W. Ross.

Wishes, expectations, and actions: A survey on price formation in

election stock markets.

Journal of Economic Behavior and Organization, 39:83-110,

1999.

- 13

-

S. French.

Group consensus probability distributions: A critical survey.

Bayesian Statistics, 2:183-202, 1985.

- 14

-

J. M. Gandar, W. H. Dare, C. R. Brown, and R. A. Zuber.

Informed traders and price variations in the betting market for

professional basketball games.

Journal of Finance, LIII(1):385-401, 1998.

- 15

-

C. Genest and J. V. Zidek.

Combining probability distributions: A critique and an annotated

bibliography.

Statistical Science, 1(1):114-148, 1986.

- 16

-

R. D. Hackathorn.

Web Farming for the Data Warehouse: Exploiting Business

Intelligence and Knowledge Management.

Morgan Kaufmann, 1998.

- 17

-

R. Hanson.

Decision markets.

IEEE Intelligent Systems, 14(3):16-19, 1999.

- 18

-

R. D. Hanson.

Could gambling save science? Encouraging an honest consensus.

Social Epistemology, 9(1):3-33, 1995.

- 19

-

E. H. Kaplan and S. J. Garstka.

March Madness and the office pool.

Management Science, 47(3):369-382, 2001.

- 20

-

M. L. Lee, W. Ling, and W. L. Low.

Intelliclean: A knowledge-based intelligent data cleaner.

In Sixth International Conference on Knowledge Discovery and

Data Mining, pages 290-294, 2000.

- 21

-

D. S. McKay, E. K. G. Jr., K. L. Thomas-Keprta, H. Vali, C. S. Romanek, S. J.

Clemett, X. D. F. Chillier, C. R. Maechling, and R. N. Zare.

Search for past life on Mars: Possible relic biogenic activity in

Martian meteorite alh84001.

Science, 273:924-930, Aug. 1996.

- 22

-

D. M. Pennock, S. Lawrence, C. L. Giles, and F. Å. Nielsen.

The power of play: Efficiency and forecast accuracy in web market

games.

Technical Report 2000-168, NEC Research Institute, 2000.

- 23

-

D. M. Pennock, S. Lawrence, C. L. Giles, and F. Å. Nielsen.

The real power of artificial markets.

Science, 291:987-988, February 9 2001.

- 24

-

C. R. Plott.

Markets as information gathering tools.

Southern Economic Journal, 67(1):1-15, 2000.

- 25

-

C. R. Plott and S. Sunder.

Efficiency of experimental security markets with insider information:

An application of rational-expectations models.

Journal of Political Economy, 90(4):663-98, 1982.

- 26

-

C. R. Plott and S. Sunder.

Rational expectations and the aggregation of diverse information in

laboratory security markets.

Econometrica, 56(5):1085-1118, 1988.

- 27

-

C. R. Plott, J. Wit, and W. C. Yang.

Parimutuel betting markets as information aggregation devices:

experimental results.

Technical Report Social Science Working Paper 986, California

Institute of Technology, Apr. 1997.

- 28

-

F. Provost and V. Kolluri.

A survey of methods for scaling up inductive algorithms.

Data Mining and Knowledge Discovery, 3(2):131-169, 1999.

- 29

-

P. Resnick and H. R. Varian.

Recommender systems.

Communications of the ACM, 40(3):56-58, 1997.

- 30

-

R. N. Rosett.

Gambling and rationality.

Journal of Political Economy, 73(6):595-607, 1965.

- 31

-

B. J. Sherrick, P. Garcia, and V. Tirupattur.

Recovering probabilistic information from options markets: Tests of

distributional assumptions.

Journal of Futures Markets, 16(5):545-560, 1996.

- 32

-

W. W. Snyder.

Horse racing: testing the efficient markets model.

Journal of Finance, 33(4):1109-1118, 1978.

- 33

-

R. H. Thaler and W. T. Ziemba.

Anomalies: Parimutuel betting markets: Racetracks and lotteries.

Journal of Economic Perspectives, 2(2):161-174, 1988.

- 34

-

D. A. Wasserman.

More than enough answers to questions nobody asked about F1Pick6,

1996.

http://www.freenet.edmonton.ab.ca/~davidwss/

[0]f1p6anal.pdf.

- 35

-

M. Weitzman.

Utility analysis and group behavior: An empirical study.

Journal of Political Economy, 73(1):18-26, 1965.

- 36

-

R. L. Winkler and A. H. Murphy.

Good probability assessors.

J. Applied Meteorology, 7:751-758, 1968.

Extracting Collective Probabilistic Forecasts from Web Games

This document was generated using the

LaTeX2HTML translator Version 2K.1beta (1.48)

Copyright © 1993, 1994, 1995, 1996,

Nikos Drakos,

Computer Based Learning Unit, University of Leeds.

Copyright © 1997, 1998, 1999,

Ross Moore,

Mathematics Department, Macquarie University, Sydney.

The command line arguments were:

latex2html -split 0 market-sim-kdd-final.tex

The translation was initiated by David Pennock on 2001-08-02

Footnotes

- ... (IEM),

- http://www.biz.uiowa.edu/iem/. Other election markets have opened in

Canada (http://esm.ubc.ca/) and Austria (http://ebweb.

[0]tuwien.

[0]ac.at/

[0]apsm/).

- ... (HSX)

- http://www.hsx.com/

- ... Ebay

- http://www.ebay.com/

- ...

Inc.

- http://www.entdata.com/

- ...

returns.

- Although cash holdings do accrue interest on HSX,

all analyses in this paper ignore any time value of Hollywood

dollars.

- ... millions).

- Movies released on holiday

weekends, and movies with substantial box office receipts prior to

wide release, may adjust differently.

- ...

(FX).

- http://www.ideafutures.com/

- ... outcomes.

- http://www.motorsport.com/compete/p6/

- ... data.

- We employ a standard least-squares regression to

obtain the best-fit line. Since the variance of data increases with

estimate magnitude, a weighted least-squares regression may be

appropriate. Ideally, weights would be inversely proportional to

variance [5], but we do not have enough data

to accurately assess variance at each point.

- ... Mojo.

- http://boxofficemojo.com/

- ... prior.

- Note that the expectation of the

Beta distribution,

, does not coincide precisely with the

observed frequency,

, does not coincide precisely with the

observed frequency,  , where

, where  is the number of successes and

is the number of successes and

the number of trials. However, as grows, the two measures

converge.

the number of trials. However, as grows, the two measures

converge.

- ... (HSBR),

- http://www.hsbr.net/

- ... 2001.

- Data for the remaining

9 races was missing.

- ... (10-6-4-3-2-1)

- We call this ``F1

style'' scoring because F1 drivers accumulate points toward their

season championship according to the same scheme. Also, F1P6 players

receive points in this manner.

- ... F1

- http://atlasf1.com/

- ... F1.

- http://galeforcef1.com/

- ...

2001.

- As of this writing, archive odds from the most recent

two races were not publicly available from Atlas F1.

- ... discovered

- http://www.ideosphere.com/fx-bin/Claim?claim=XLif

David Pennock

2001-08-02